Here's a sentence that stops most future expats mid-plan: the day you become a non-resident of Canada, the CRA deems you to have sold nearly everything you own — and taxes you on the gains, even though you didn't sell a thing and no money changed hands.

It's called the departure tax, and it isn't a penalty, a punishment, or an exit fee for disloyalty. It's a deemed disposition under section 128.1(4) of the Income Tax Act, and the logic behind it is almost fair: Canada taxed you on your worldwide income while you lived here, so it wants its share of the gains that built up on your watch — settled now, before you and your portfolio disappear into another country's tax system.

Almost fair. Because in practice, the departure tax lands on people who never saw it coming: the retiree whose "boring" index funds quietly doubled, the couple who assumed their house covered everything, the professional who found out about Form T1161 eighteen months too late and got fined for a form that owed no tax at all.

Here's how the whole machine works: what's deemed sold, what's spared, what the bill actually looks like, and the elections that let you postpone paying it — sometimes for decades.

First things first: this only happens if you actually leave

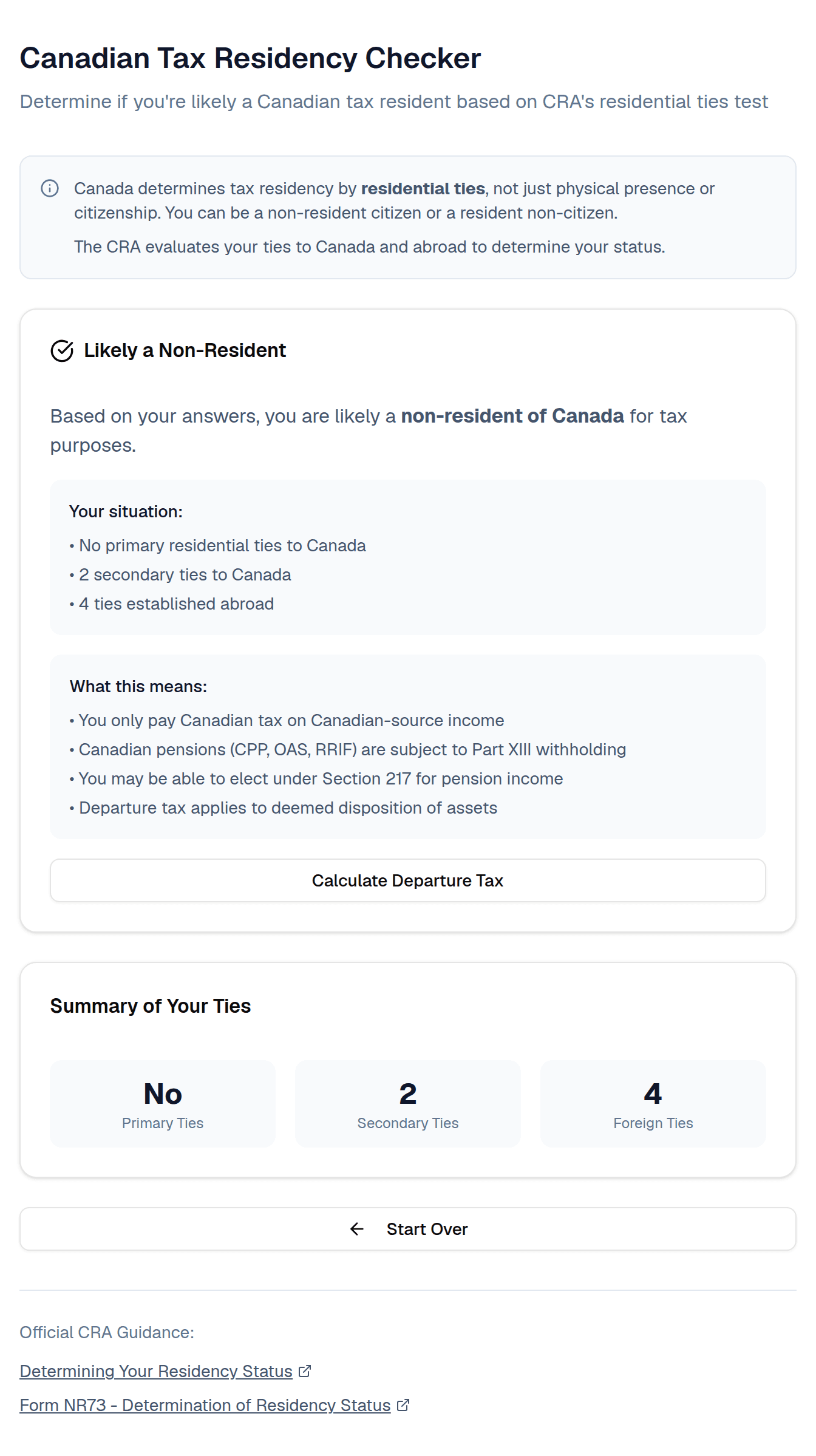

The departure tax is triggered by one event: the day you cease to be a tax resident of Canada. Not the day your flight leaves, not the day you get your new visa — the day your residential ties shift enough that Canada no longer considers you a resident.

That's a facts-and-circumstances test, not a checkbox. The CRA looks at primary ties (a home available to you in Canada, a spouse or dependants still here) and secondary ties (bank accounts, a provincial driver's licence, provincial health coverage, memberships, a car in your brother's garage). Keep a primary tie and you're almost certainly still a resident — still taxed on worldwide income, and no departure tax yet, because you haven't departed.

Our tax residency checker walks the CRA's ties test in about a minute:

Two things to note before moving on:

- Your departure date matters enormously. It sets the valuation date for every deemed disposition, splits your final tax return into a resident part and a non-resident part, and starts the clock on non-resident withholding for your pensions and RRIFs. Document it — lease signed abroad, ties severed, family moved — like you might one day have to prove it. Because you might.

- Think twice before filing Form NR73. The CRA's residency-determination questionnaire is optional, its answer doesn't bind the CRA, and it gives them a detailed picture of your ties. Most emigrants skip it and simply declare their departure date on the final return.

What the CRA pretends you sold (and what it doesn't)

On your departure date, you're deemed to have disposed of most capital property at fair market value and instantly re-acquired it at that same value. Any accrued gain becomes taxable on your final resident return. The list of what's in and what's out is where the real planning lives.

Deemed sold on departure

- Non-registered investments — stocks, ETFs, mutual funds in taxable accounts. This is the big one for most people.

- Foreign real estate — the condo in Portugal counts, even though it's already abroad.

- Private business interests — shares of your corporation, partnership interests.

- Crypto and other capital property — collectibles, precious metals, and most other property with an accrued gain.

Not deemed sold on departure

- Canadian real estate. Real property in Canada is taxable Canadian property — Canada can tax it whenever you actually sell, no matter where you live, so it doesn't need to settle up at departure. Your rental property and cottage cross the border with you untouched (for now).

- RRSPs and RRIFs. Registered plans aren't deemed disposed. They stay intact and get taxed later through non-resident withholding on withdrawals — a different regime, with its own elections.

- TFSAs and FHSAs. No deemed disposition, and Canada keeps treating the TFSA as tax-free. Two warnings, though: you're not supposed to contribute once you're a non-resident — and doing so creates tax problems in your new country — which probably doesn't recognize the wrapper anyway and may treat the TFSA as an ordinary taxable account.

- Your principal residence. The principal residence exemption shelters the gain for the years you lived in it. (Whether to sell before or after you leave is its own decision — more below.)

- CPP, OAS, and pension rights. Pensions, annuities, and similar rights are exempt from the deemed disposition. Nothing to deem.

One more escape hatch worth knowing: short-term residents — in Canada 60 months or less during the 10 years before departure — are generally exempt on property they owned before they became residents. If you came for a five-year work stint and are heading home, the departure tax may barely touch you.

The math: your gains get stacked on top of your income

The deemed gains aren't taxed at some special flat rate. They're capital gains on your final resident return: 50% of the gain is included in income, and that taxable half gets stacked on top of everything else you earned in the departure year — salary, business income, the works. Which means the same portfolio costs more to exit in a year you also earned a full salary than in a year you didn't. Timing is a lever.

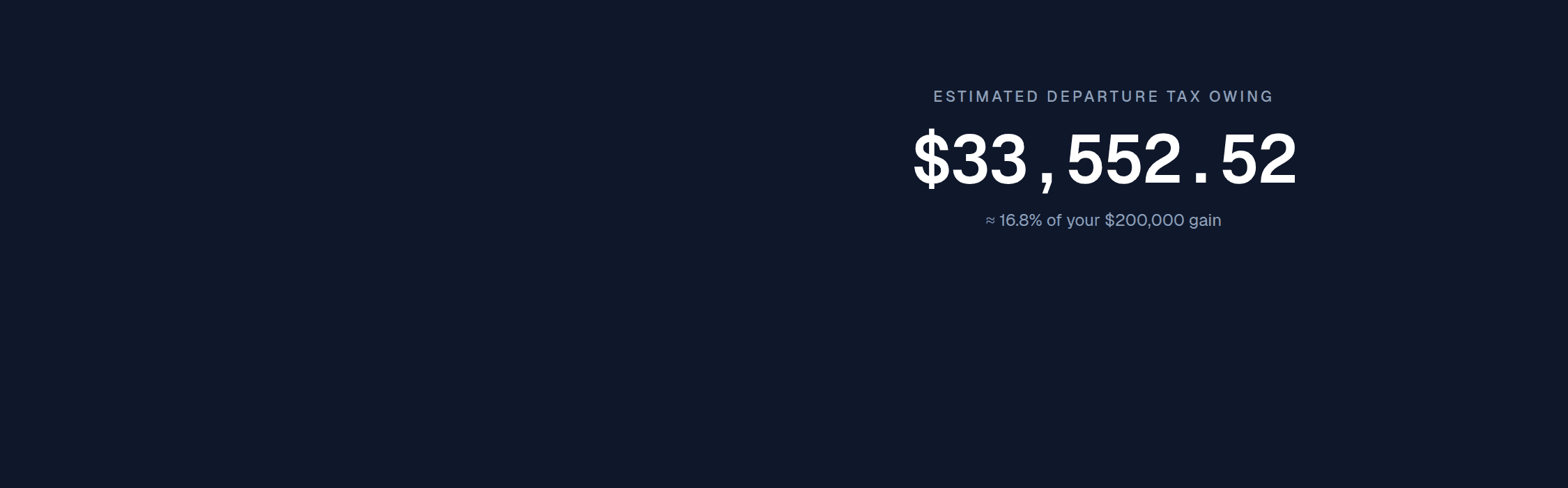

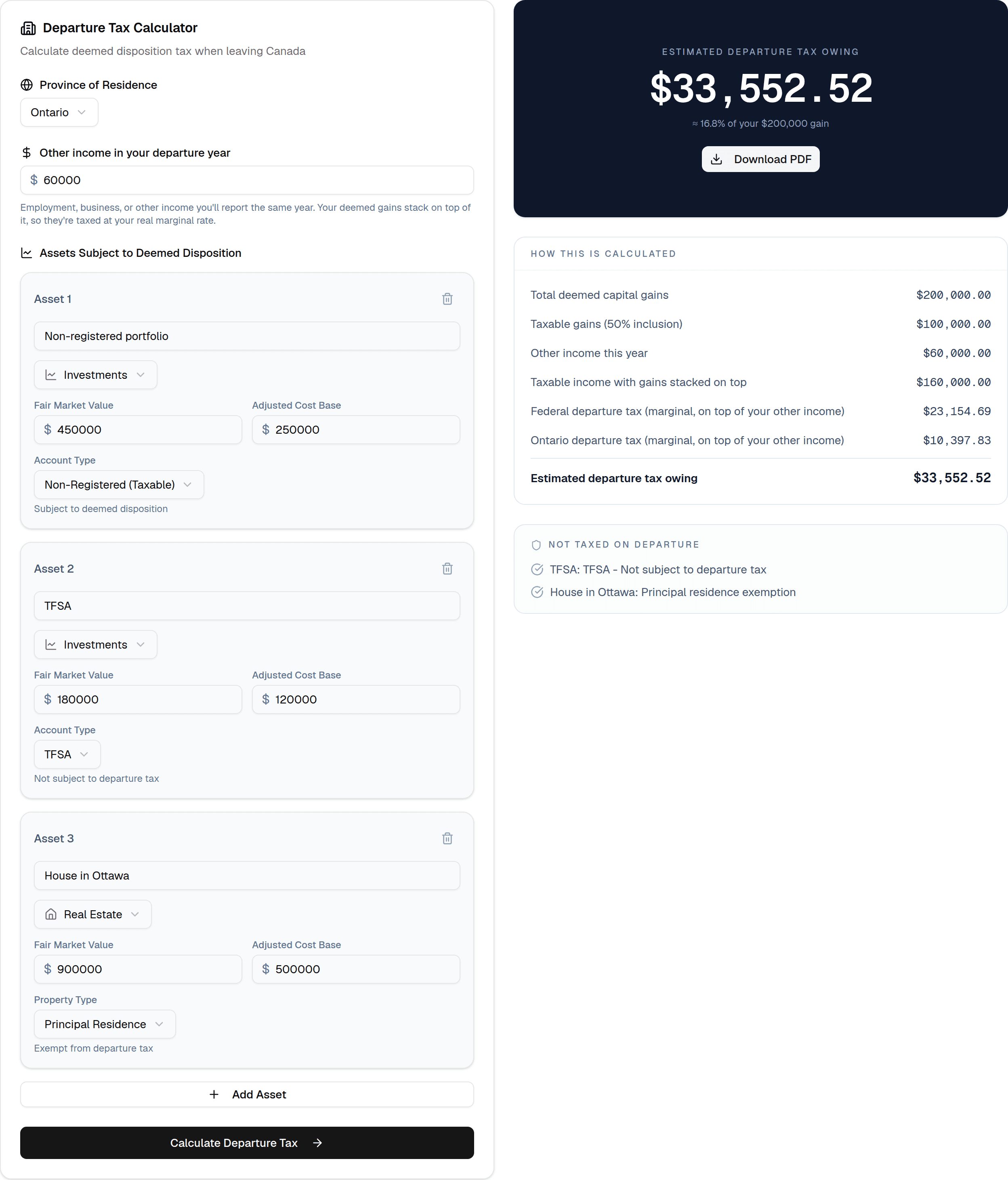

Here's a concrete scenario in our departure tax calculator: an Ontario resident with $60,000 of other income in the departure year, a non-registered portfolio worth $450,000 that cost $250,000, a TFSA, and a principal residence:

The $200,000 paper gain on the portfolio produces a departure tax bill of roughly $33,500 — about 17 cents per dollar of gain — while the TFSA and the house pass through untouched. No cash was received. The bill is real anyway.

The calculator handles every province and territory, stacks the gains on your other income so you see the true marginal cost, and shows the whole computation line by line. Run your own numbers before you pick a departure date — a January departure and a December departure can be thousands of dollars apart.

The paperwork: three forms, one famous trap

The departure tax lives on your final resident tax return, due April 30 of the year after you leave. Three forms do the work:

- Form T1161 — List of Properties by an Emigrant. If everything you own on departure day is worth more than $25,000 in total (excluding cash, registered plans, and small personal-use items), you must file this inventory of your property. Here's the trap: T1161 is required even if you owe zero departure tax. It's an information form, and the penalty for missing it is $25 a day, up to $2,500 — assessed cheerfully on people whose actual departure tax was nil. This form is, by a wide margin, the most common departure-tax mistake we see.

- Form T1243 — Deemed Disposition of Property. The actual calculation: each deemed-disposed asset, its fair market value on departure day, its adjusted cost base, and the resulting gain. This is why you want valuations dated to your departure date — brokerage statements, an appraisal for the foreign property, a professional valuation for private company shares. Reconstructing fair market value two years later is expensive guesswork.

- Form T1244 — the deferral election. The quiet hero of the whole regime, which deserves its own section.

The election almost nobody uses: defer the bill, interest-free

Owing $33,500 on gains you haven't realized is exactly as painful as it sounds — the deemed disposition creates a tax bill but no cash to pay it with. Parliament knew, so the Act contains a remarkable fix: elect under Form T1244 and you can defer paying the departure tax until you actually sell the property. No payments, and — this is the remarkable part — no interest, however long the deferral runs. Sell the shares twelve years from now, pay the departure tax then, and the CRA charges you nothing for the wait.

The mechanics:

- File T1244 with your final return, electing to defer the tax on the deemed disposition.

- No collateral is needed on the first $100,000 of capital gains. Above that, once the federal tax you're deferring passes $16,500, the CRA wants collateral — which can be as simple as a charge over your brokerage account — in place by April 30 of the year after departure.

- The deferral runs indefinitely. The deferred tax comes due, asset by asset, when you actually dispose of each one, when you die, or when you return to Canada.

And the companion rule for the changed-my-mind crowd: if you return to Canada while still owning the property, you can generally elect to unwind the deemed disposition — as if you'd never left. Confirm the mechanics with a professional before you move back. The departure tax is designed to tax leavers on what they take, not to punish people for trying life abroad and coming home.

The house question: sell before you go, or after?

Your principal residence deserves its own decision, because the exemption doesn't travel well.

The principal residence exemption shelters the gain for the years the home was your principal residence — and a year generally only counts if you were resident in Canada during that year. Sell while you're still a resident and the gain is typically fully sheltered (the exemption formula's extra year usually covers a sale soon after departure too). Hold the house for years after you leave and the arithmetic shifts: the post-departure years aren't covered, so a growing slice of the eventual gain becomes taxable — and since Canadian real estate isn't deemed disposed at departure, that reckoning happens on the actual sale, under non-resident rules.

Selling as a non-resident is also simply more annoying: the buyer's lawyer must hold back a chunk of the price (typically 25% of gross proceeds) until you produce a section 116 clearance certificate from the CRA. You'll get the excess back after filing, but only after months of your money sitting in trust.

None of this means "always sell before leaving" — a hot rental market, a possible return to Canada, or a plan to sell within a year of departure can all tip the other way. It means the house belongs in the departure plan, not in the "deal with it later" pile. (The same goes for your will and powers of attorney, which may not survive the move either.)

How to actually plan for this

Pulling it together, the departure tax playbook looks like this:

- Confirm you'll genuinely be a non-resident. Run the residency checker, sever the primary ties, and document your departure date. No non-residency, no departure — just worldwide taxation with extra steps.

- Inventory everything before you book flights. What's deemed disposed, what's exempt, what's sitting on a big accrued gain. This is also the moment to find your adjusted cost bases, while the records are still easy to reach.

- Ask your brokerage what happens to your account — before you decide to hold. Most Canadian platforms restrict ("liquidate only") or close non-resident accounts, and that operational reality often settles the sell-versus-hold question before the tax math gets a vote. If you'll be forced to liquidate anyway, selling while you're still a resident — on your own timing — beats selling on a 30-day deadline from abroad.

- Run the numbers on timing. Gains stack on top of departure-year income, so leaving in a low-income year — or realizing some gains gradually in the years before departure, or harvesting losses against the deemed gains — can shrink the bill. Every full tax year between now and departure is another run up the graduated brackets. Our calculator makes the comparison a two-minute job.

- Get departure-day valuations. Statements, appraisals, a valuation for the business. Dated evidence now beats forensic reconstruction later.

- Decide on the deferral. If the bill is painful and the assets are keepers, T1244 postpones it interest-free. If the federal amount tops $16,500, budget time to arrange security.

- File the trio. Final return by April 30, T1243 for the calculation, and T1161 even if you owe nothing — that $2,500 penalty is the cheapest mistake to avoid in this entire process.

- Check the other side. Some countries give arriving residents a step-up in cost base to fair market value (so the gain Canada just taxed never gets taxed again); others don't, and the treaty fine print decides. This is the one step where a cross-border accountant earns their fee several times over.

Our leaving Canada checklist folds all of this into the broader departure sequence — banks, CRA notifications, health coverage, the lot.

The bottom line: The departure tax isn't a reason to stay, and for most people it isn't even the biggest number in the move — but it is the least forgiving surprise. The day you become a non-resident, Canada settles the tab on your paper gains: non-registered investments in, registered plans and Canadian real estate out, everything valued as of one specific day. The people who get hurt aren't the ones with big portfolios. They're the ones who found out at filing time — after the valuation date had passed, after the timing levers had expired, and occasionally $2,500 poorer for skipping a form that owed no tax at all. Find out before you leave. It's cheaper.