There's a persistent fantasy in every expat Facebook group, and it goes like this: "Once I'm a non-resident, my Canadian money comes to me tax-free. Canada can't touch me anymore."

It's wrong. Confidently, expensively wrong.

But the opposite belief — quietly held by thousands of Canadian retirees abroad — is wrong too: "Canada takes 25% of my pension no matter what. That's just the price of leaving." Also wrong, and this version of wrong can cost you thousands of dollars a year that the CRA would have happily given back if you'd asked correctly.

After watching both mistakes play out over and over, here's the full picture: what actually happens to Canadian-source income when you become a non-resident, the moment the tax starts (it's earlier than you think), and the two elections — section 217 and Form NR5 — that most people have never heard of.

Myth #1: "Money from Canada is tax-free once I leave"

The misconception: Becoming a non-resident ends your relationship with the CRA. Your CPP lands in your Portuguese bank account untouched, your RRIF withdrawals arrive whole, and Canadian tax is somebody else's problem now.

The reality: Becoming a non-resident doesn't end the relationship. It changes the collection method.

As a Canadian resident, you file a return every April and settle up. As a non-resident, Canada switches to something far more efficient: it takes its cut before the money ever reaches you. This is Part XIII of the Income Tax Act, and it covers most of the Canadian-source income an expat keeps receiving:

- CPP and OAS

- RRSP and RRIF withdrawals

- Registered pension payments and annuities

- Dividends from Canadian companies

- Rent from your Canadian property

The default rate is a flat 25% of the gross amount. Not 25% of your profit, not 25% after deductions — 25% off the top of every single payment, withheld by the payer and remitted straight to the CRA. If you live in a country with a Canadian tax treaty, the rate on many income types drops (15% is common; a few treaties take CPP and OAS all the way to zero). But the mechanism is the same: the tax comes out at source, automatically, forever.

What confuses people is that the fantasy is partly true, which keeps it alive. Once you're genuinely a non-resident, Canada stops taxing your worldwide income — your salary in Dubai and your dividends from a US brokerage are no longer Canada's business. A few kinds of Canadian income really do flow tax-free: arm's-length interest (bank accounts, GICs, most bonds) has been exempt from withholding since 2008, and Canada generally doesn't tax non-residents on capital gains from listed stocks, ETFs, or mutual funds — partly because it already settled that score through departure tax on the way out.

So: interest and stock gains, mostly fine. Pensions, RRIFs, dividends, and rent? Canada is standing at the door with its hand out, and it gets paid before you do.

The part nobody tells you: updating your address is the tax event

Here's the mechanical detail that catches almost everyone.

You land in your new country, get settled, and eventually do the responsible thing: you call your bank, your brokerage, and Service Canada to update your address and mention you've moved abroad. You're expecting… nothing, really. Address updates are clerical.

Not this one. The moment a Canadian financial institution learns you're a non-resident, non-resident withholding starts. There's no separate registration, no form you sign to "opt in" to Part XIII, no grace period. Your profile flips to non-resident, the system applies the withholding rate for your country of residence, and your next RRIF payment arrives 25% (or 15%) lighter. People stare at that first shrunken deposit convinced the bank made an error. It didn't. That's the system working exactly as designed.

And before you ask — no, the answer is not "then I just won't tell them." That's not a loophole; it's a liability with your name on it, twice over:

- The correct tax is owed whether or not it was withheld. If your payer under-withholds because it didn't know you'd left (or had the wrong country on file), the CRA can assess you for the shortfall. The tax doesn't disappear; it just arrives later, with interest and a worse attitude.

- Treaty rates only work when the payer knows where you live. Your bank can't apply the Canada–Mexico treaty rate if it thinks you're still in Mississauga. Telling your payers promptly — you're a non-resident, and which country you're a resident of — is how you get the lower rate you're actually entitled to.

So the address call isn't optional, and it isn't clerical. It's the first real step of your non-resident tax life. One more wrinkle for OAS recipients: depending on your country, you may also need to file the yearly OAS Return of Income to keep the payments flowing at all — "no Canadian tax return" was never quite the whole story.

Myth #2: "Withholding is just what it costs — there's nothing you can do"

The misconception: The flat withholding is the final word. Every Canadian abroad pays it, it's the cost of doing business, close the file.

The reality: For pension-type income, the flat withholding is the default, not the only option. And for a lot of retirees, it's a terrible default.

Think about what 25% flat actually means. A Canadian resident with $30,000 of pension income pays very little income tax — graduated rates start at zero and personal credits soak up much of the rest. A non-resident with the same $30,000 hands over a flat 25% with no brackets and no credits. Same pension, radically different treatment — purely because of the collection method.

Parliament knew this was rough, so the Income Tax Act contains a fix that shockingly few people use: the section 217 election.

Route two: the section 217 election

Section 217 lets a non-resident receiving certain pension-type income — CPP, OAS, RRSP and RRIF withdrawals, registered pensions, annuities — elect to file a Canadian return and be taxed at the same graduated rates as a resident, personal credits included, instead of the flat withholding.

Note the wording: pension-type income. The election is built for people whose income is predominantly pension-like, in two senses. First, only those income types can go into it — dividends can't (their withholding is final; no election exists), interest doesn't need it, and rent has its own regime. Second, the personal credits that make the election worthwhile are only fully available when the income you're electing on makes up at least 90% of your worldwide income for the year. A retiree living on CPP, OAS, and a RRIF clears that bar easily. Someone earning a good salary in Dubai with a small Canadian pension on the side doesn't — the credits get prorated away, and the election usually does nothing for them.

The process, end to end:

- During the year, the full withholding comes off every payment, same as always. Nothing changes at the source.

- After year-end, you file a section 217 return. The deadline is June 30 of the following year.

- The CRA recalculates your tax at graduated rates. If the result is lower than what was withheld, the difference comes back as a refund.

Two things make this election unusually forgiving. First, it's optional and self-selecting: if the graduated calculation doesn't beat the withholding — which is typically the case at higher incomes, where flat 25% is a bargain — the CRA simply disregards the election and the withholding stands. There is no penalty for running the numbers. Second, it works retroactively on a year that's already happened: even if you've been abroad for years paying full freight, you can elect for this year, this coming June.

The catch is cash flow. The full withholding still comes off all year, and the refund only arrives after the CRA assesses your return — money withheld in January can take well over a year to find its way back. Which brings us to the third route.

Route three: Form NR5 — the same savings, without the wait

Form NR5 is the section 217 election's impatient sibling. Instead of overpaying all year and reclaiming the difference, you ask the CRA in advance for permission to have less withheld in the first place.

The process:

- You file Form NR5 before your first payment, or by October 1, estimating your income for the year.

- If the CRA approves — and one approval generally covers up to five years — it authorizes your Canadian payers to withhold at your lower estimated section 217 rate instead of the flat rate.

- In exchange, you must file the section 217 return by June 30 every year the approval is in effect. This is not optional. Skip a year and the CRA can cancel the reduction, and you're back to full withholding.

Run correctly, the NR5 route lands in the same place as section 217 alone — the same recalculated tax — but the right amount is collected as you go, in every payment, with no refund to chase. For a retiree living month to month on pension income, that difference isn't cosmetic. It's groceries.

And rent? Rental income lives in its own parallel universe — the section 216 election to be taxed on net rather than gross rent, with Form NR6 playing the NR5 role — but that's its own article.

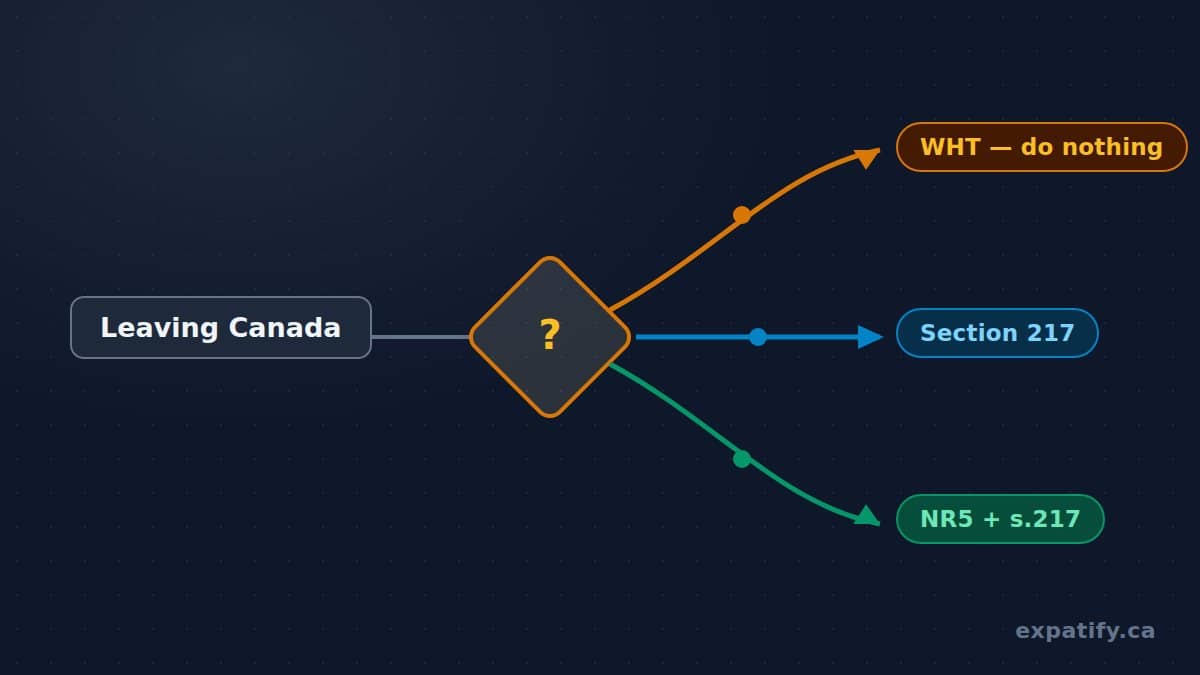

Which route is yours? Follow the flowchart

Three routes, each with its own filings, deadlines, and failure modes:

- Do nothing. Withholding comes off every payment and is generally your final Canadian tax — no Canadian return. Usually right at higher incomes, and unbeatable on paperwork.

- Section 217 alone. Full withholding all year, file by June 30, refund after assessment. Right for modest pension incomes when the payments have already started.

- NR5 + section 217. File ahead, get approved, keep more of every payment — and commit to filing every year. Right for modest pension incomes when you can plan before the payments begin.

Here are all three routes as flowcharts — one tab per route, each walking from the first step to the final outcome, including the branches where things go wrong: the under-withholding that stays your problem, the election that gets disregarded, the NR5 reduction that gets cancelled for a missed return.